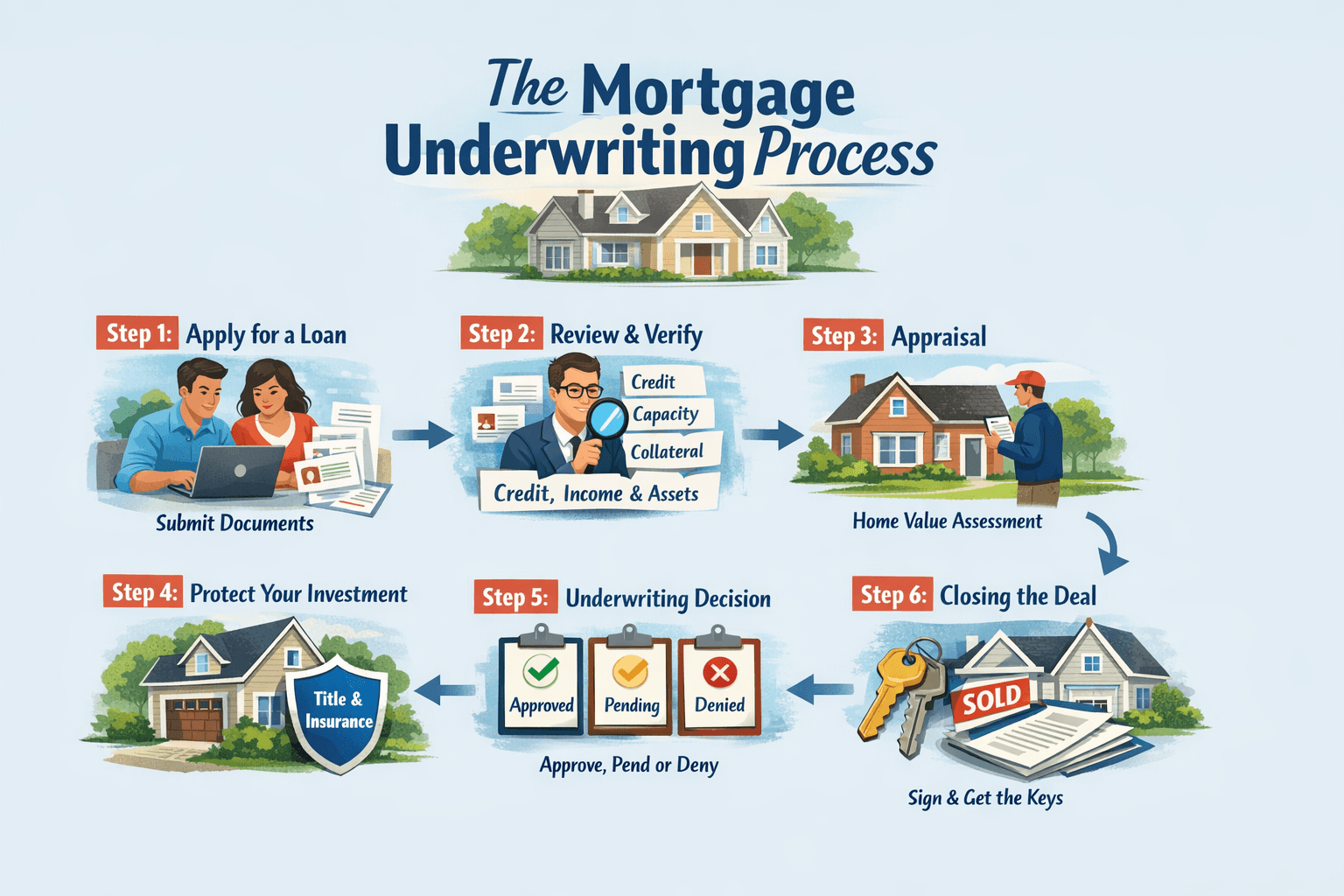

How AI Is Transforming Mortgage Underwriting Management—Without Increasing Risk

Mortgage underwriting managers sit at the center of risk, operations, and growth. They’re responsible not only for approving loans, but for building systems, teams, policies, and controls that scale—while staying compliant in one of the most regulated industries in the world.

As loan volumes fluctuate, guidelines evolve, and staffing challenges persist, underwriting leaders are being asked to do more with less, move faster, and reduce defects—without sacrificing quality.

This is exactly where AI, when implemented correctly, becomes a force multiplier for underwriting managers. Not to replace judgment—but to protect it, scale it, and make it consistent.

This article breaks down:

What mortgage underwriting managers actually do day-to-day

Why those responsibilities are increasingly difficult

How AskBobAI helps underwriting managers operate faster, smarter, and safer

What Mortgage Underwriting Managers Actually Do (Beyond “Approving Loans”)

A Wholesale Mortgage Underwriting Manager is not just an underwriter with a title. It’s a senior leadership role responsible for shaping the credit culture of the company.

Based on the job responsibilities you outlined, underwriting managers typically own six major areas:

1. Credit Risk Policy & Internal Controls

Underwriting managers:

Establish and enhance credit risk policies, procedures, and controls

Align underwriting decisions with the company’s risk appetite

Own internal and external credit guidelines, matrices, and overlays

Partner with compliance, QC, and risk to remediate defects

This requires deep knowledge of:

FNMA, FHLMC, USDA, Non-QM, Jumbo, and investor overlays

Regulatory expectations and audit defensibility

How policies are interpreted—not just written

The challenge:

Guidelines live across PDFs, investor sites, emails, internal matrices, and institutional knowledge inside senior underwriters’ heads.

2. Workflow & Operations Management

Underwriting managers oversee:

End-to-end underwriting workflow

Turn times, capacity planning, and pipeline health

Bottlenecks between sales, processing, underwriting, and closing

System usage (AUS, LOS, MeridianLink / Lending QB)

They’re expected to:

Optimize processes

Improve efficiency

Enhance customer and broker experience

The challenge:

Underwriters waste time searching for answers, reworking files, and escalating questions that should be standardized.

3. Senior-Level Decision Support

Underwriting managers are the final escalation point for:

Policy interpretation questions

Product eligibility edge cases

Investor exceptions

Systemic underwriting inconsistencies

They are the:

“Most senior-level resource” for underwriting questions

Trusted voice for sales, brokers, and executives

The challenge:

The same questions get asked repeatedly, across teams, channels, and time zones—pulling managers out of strategic work.

4. Staffing, Recruiting & Training

Underwriting managers are responsible for:

Staffing recommendations and workforce planning

Interviewing and hiring underwriters

Designing onboarding programs

Developing ongoing training initiatives

Standardizing underwriting decision quality

The challenge:

Training is often manual, inconsistent, and dependent on shadowing senior underwriters—creating variability and risk.

5. Investor & Agency Relationships

Underwriting managers:

Maintain agency and investor relationships

Stay ahead of guideline changes and market trends

Communicate issues with urgency and professionalism

Anticipate upcoming opportunities and risks

The challenge:

Investor updates are frequent, nuanced, and easy to misinterpret—especially when guidance changes mid-cycle.

6. Executive & Cross-Functional Leadership

Underwriting managers:

Participate in senior executive meetings

Align underwriting objectives with sales and operations

Balance growth goals with credit discipline

The challenge:

Leadership decisions depend on accurate, current, and shared understanding of policy and performance.

Why This Role Is Getting Harder (Not Easier)

Even highly experienced underwriting managers face structural challenges:

📄 Guidelines are fragmented and constantly changing

🧠 Institutional knowledge is trapped in people’s heads

⏱ Underwriters spend too much time searching instead of deciding

🔁 The same questions are answered repeatedly

📉 Inconsistent interpretations lead to defects and buybacks

🧑🏫 Training new underwriters takes too long

Traditional systems (LOS, AUS, PDFs, SharePoint folders) store information—but don’t make it usable in real time.

How AskBobAI Helps Mortgage Underwriting Managers

AskBobAI is an enterprise AI knowledge platform built for regulated industries like mortgage lending.

It doesn’t replace underwriting judgment.

It scales access to the right information, at the right time, with proof.

Here’s how it directly supports underwriting managers.

1. One Source of Truth for Credit Policies & Guidelines

AskBobAI centralizes:

Agency guidelines (FNMA, FHLMC, USDA)

Non-QM and Jumbo investor matrices

Internal overlays and policies

Credit memos and procedural updates

Underwriters can ask:

“Is this borrower eligible under FNMA with 1099 income?”

“What’s our current jumbo overlay for reserves?”

“Which investor allows this exception?”

AskBobAI responds with:

Clear answers

Exact source citations

Current-version awareness

Result for managers:

Fewer escalations. More consistency. Lower defect rates.

2. Faster, More Consistent Underwriting Decisions

Instead of:

Searching PDFs

Emailing managers

Guessing interpretations

Underwriters get instant, standardized answers—backed by approved documents.

Result for managers:

Improved turn times

Reduced rework

Less decision variance across underwriters

3. Scalable Onboarding & Training

AskBobAI becomes a virtual underwriting mentor for new hires.

New underwriters can:

Ask real-world underwriting questions

Learn policy interpretation with citations

Self-serve instead of interrupting senior staff

Managers can:

Standardize training content

Reduce ramp time

Preserve institutional knowledge even when staff changes

Result for managers:

Training scales without sacrificing quality.

4. Reduced Dependency on Senior Escalations

AskBobAI captures:

Prior interpretations

Approved policy explanations

Clarifications managers have already given

This prevents:

Re-answering the same questions

Bottlenecking senior leadership

Knowledge loss when people leave

Result for managers:

More time for strategy, risk oversight, and leadership.

5. Audit-Ready, Defensible Answers

Every AskBobAI response is:

Source-backed

Version-aware

Permission-controlled

This supports:

Internal QC

External audits

Regulatory exams

Investor reviews

Result for managers:

Confidence that underwriting decisions are defensible—not just fast.

6. Better Cross-Team Alignment

AskBobAI can be used by:

Underwriting

Sales

Operations

Compliance

Secondary / Capital Markets

Everyone gets answers from the same source of truth.

Result for managers:

Fewer miscommunications. Stronger alignment between growth and risk.

Why AI for Underwriting Managers Is No Longer Optional

Mortgage underwriting managers are expected to:

Improve efficiency

Reduce defects

Scale teams

Maintain compliance

Support growth

Without AI, this depends heavily on:

Manual effort

Individual heroics

Tribal knowledge

With AskBobAI, underwriting managers get:

Consistency without rigidity

Speed without shortcuts

Scale without added headcount

Confidence without guesswork

Final Takeaway: AI Is Becoming the Knowledge Layer for Underwriting Teams

Mortgage underwriting managers don’t need more dashboards, more email threads, or more fragmented guideline documents.

They need clarity, consistency, and confidence in every credit decision their teams make.

When underwriting teams spend less time searching for answers and more time applying sound judgment, the entire organization benefits. Turn times improve, defects decline, training accelerates, and underwriting leaders can focus on strategy instead of constant escalations.

AI does not replace underwriting expertise. It protects it, scales it, and makes it accessible across the organization.

With AskBobAI, underwriting managers gain a trusted knowledge system that helps their teams make faster decisions, apply guidelines consistently, and operate with the level of control that regulators, investors, and executives expect.

In an industry where precision, speed, and defensibility all matter, the organizations that succeed will be the ones that empower their underwriting teams with the right intelligence at the right time.

Frequently Asked Questions (FAQ)

What does a mortgage underwriting manager actually do?

A mortgage underwriting manager oversees the underwriting department and ensures loan decisions follow agency guidelines, investor requirements, and internal credit policies. Their responsibilities typically include managing underwriting staff, maintaining credit policies, resolving complex loan scenarios, overseeing workflow efficiency, coordinating with compliance and QC teams, and ensuring underwriting decisions are consistent and defensible.

Why is mortgage underwriting becoming more difficult?

Mortgage underwriting has become more complex due to constantly changing guidelines, multiple investor overlays, regulatory scrutiny, and operational pressures to reduce turn times. Underwriters must interpret large volumes of documentation across many sources, which increases the risk of inconsistent decisions and operational bottlenecks.

Can artificial intelligence replace mortgage underwriters?

No. AI is not designed to replace underwriting judgment. Instead, it supports underwriters by providing instant access to guidelines, policies, and historical interpretations. This allows underwriters to make better decisions faster while maintaining full control over credit approvals.

How can AI improve mortgage underwriting operations?

AI can help underwriting teams by:

• Instantly answering guideline and policy questions

• Reducing time spent searching through PDFs and investor websites

• Standardizing policy interpretations across teams

• Accelerating training for new underwriters

• Reducing escalations to senior underwriting leadership

By improving access to knowledge, AI helps underwriting teams operate faster while maintaining compliance.

How does AskBobAI support mortgage underwriting managers?

AskBobAI acts as a centralized knowledge system that allows underwriting teams to ask questions and receive answers grounded in approved documents and policies. It helps underwriting managers scale their teams by making institutional knowledge accessible, reducing repetitive questions, improving training, and ensuring underwriting decisions are supported by clear source documentation.

Is AI safe for regulated industries like mortgage lending?

Yes—when implemented correctly. Enterprise AI platforms like AskBobAI are designed to operate within permission-controlled environments, use verified internal documents as their knowledge source, and provide cited answers that support auditability and compliance requirements.