AI for Mortgage Processors

What if every file you touched was complete, consistent, and ready for underwriting the first time?

No missing documents. No last-minute conditions. No back-and-forth just to get a file

“submission ready.”

Because if you’re a mortgage processor, you know that’s not how it works today.

Files come in incomplete. Documents don’t match. Borrowers send partial information. Loan officers are moving fast, and somewhere in the middle of all that, you’re expected to organize everything, fix the gaps, and get the loan ready for underwriting—on time.

That’s the job. And that’s exactly where AI starts to matter.

What a Mortgage Processor Actually Does

At a high level, a mortgage processor is responsible for assembling, organizing, and preparing a loan file so it can be approved by underwriting.

But in reality, the role is much more hands-on and detail-driven.

You’re collecting financial documents—tax returns, W-2s, bank statements, proof of assets—and making sure everything is accurate and complete. You’re reviewing credit reports, identifying discrepancies, and requesting explanations when something doesn’t add up. You’re ordering appraisals and title work, tracking deadlines, and coordinating with multiple parties to keep the loan moving forward.

And most importantly, you’re acting as the bridge between the loan officer and the underwriter.

If the file isn’t clean, the underwriter can’t move forward.

Which means everything depends on how well the file is prepared.

How Many Mortgage Loans Can One Processor Handle?

How many mortgage loans a processor can realistically handle varies widely because the workload depends on several operational factors. The technology stack a company uses, the efficiency of its workflow, the level of organization within the company, and the experience of the loan officers all play major roles. Responsibilities also matter—processors who handle everything from disclosures through funding will naturally carry fewer files than those who only manage part of the process.

In practice, pipeline size typically falls within a range depending on the type of lender and operational structure:

Mortgage broker processors: Typically manage 30–40 active files at a time.

Direct lender processors: Often handle up to around 70 files, thanks to more standardized processes and internal support teams.

Highly optimized operations: With strong systems and clear workflows, some processors report managing even larger pipelines.

Ultimately, the real bottleneck is rarely the processor’s personal capacity. It’s the combination of technology, team structure, workflow design, and operational discipline within the organization.

The Real Bottleneck in Processing Isn’t Effort—It’s Inconsistency

Processing isn’t hard because people aren’t working hard enough. It’s hard because every file is different. One borrower submits everything upfront. Another sends documents in pieces. One file is straightforward. The next has layered income, credit issues, or missing information.

So what happens?

You:

Chase documents

Re-check calculations

Compare information across files

Go back to the borrower or loan officer for clarification

Not once—but multiple times per file. And that creates delays. Not because the team isn’t capable. But because the process itself is fragmented.

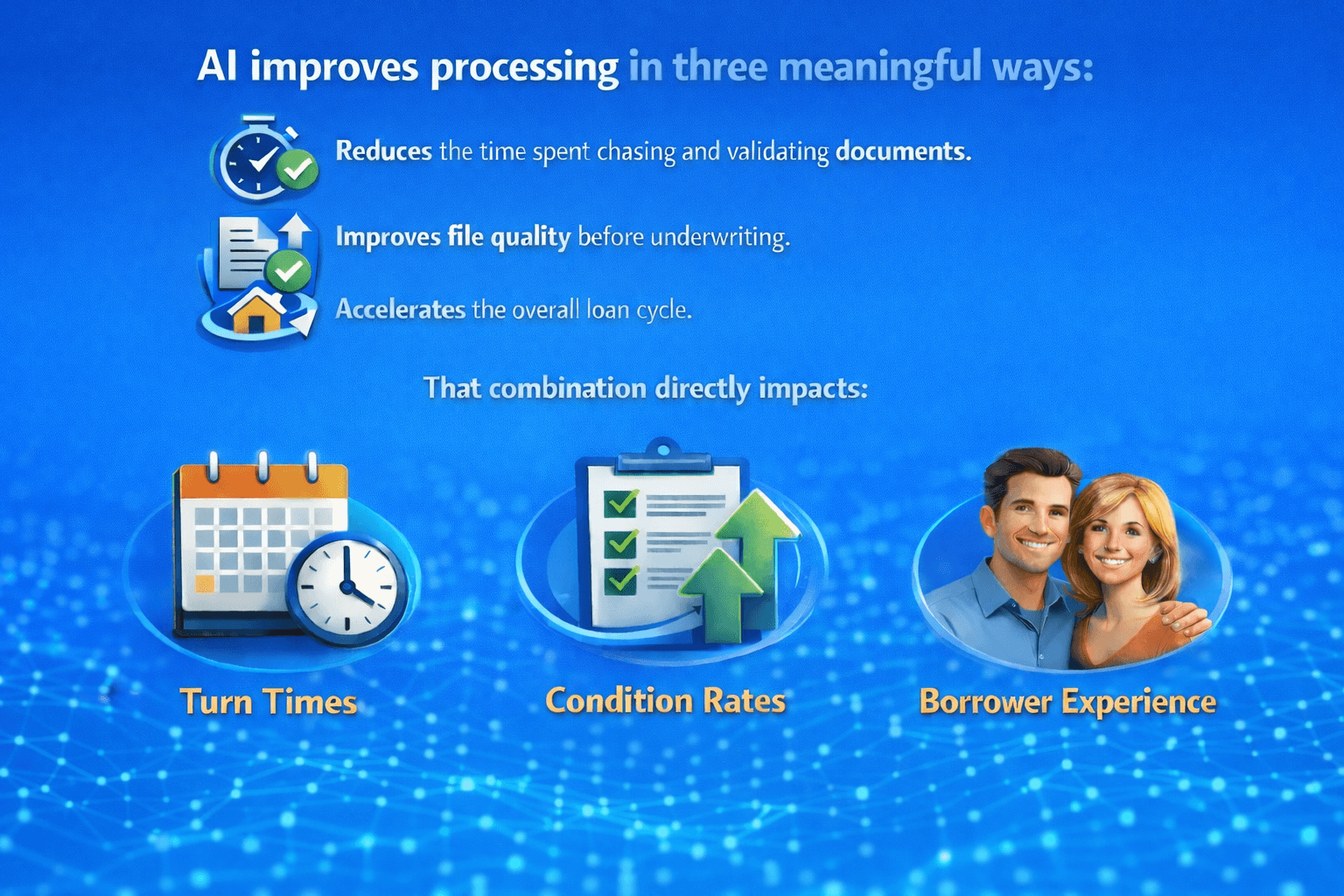

Where AI Changes the Game for Mortgage Processors

The question is no longer just how many loans a processor can handle, but how many loans a processor should need to handle at all when AI is introduced into the workflow. Traditional processing capacity is limited by manual tasks—collecting documents, checking guidelines, chasing conditions, answering loan officer questions, and organizing files. AI changes this dynamic by automating many of these repetitive steps, allowing processors to focus on exceptions, borrower communication, and final review rather than administrative work.

When AI is integrated into the mortgage workflow, the capacity equation shifts dramatically:

Document review and classification can be automated.

Guideline and scenario questions can be answered instantly by AI.

Condition tracking and follow-ups can be generated automatically.

File organization and data extraction can occur without manual entry.

As a result, processors are no longer constrained by the same operational bottlenecks. Instead of asking “How many files can one processor carry?”, organizations begin asking a different question: “How much of the processing work can AI handle before a human needs to step in?”

What This Looks Like in Practice (AskBob Scenarios)

Let’s walk through how this plays out in real workflows.

Scenario 1: Document Collection and Validation

A borrower uploads documents. Instead of manually reviewing each one line by line, AskBob can:

Identify required documents based on the loan type

Flag anything missing

Highlight inconsistencies across income, assets, or liabilities

So instead of discovering issues later, you catch them upfront.

Scenario 2: Credit Review and Explanation Gaps

When reviewing a credit report, processors often need to:

Identify late payments or collections

Request letters of explanation

Ensure everything aligns with the file

AskBob can surface:

Key credit risks

Missing explanations

Potential red flags before submission

This reduces the back-and-forth after underwriting.

Scenario 3: Appraisal and Title Review

Appraisals and title reports are often long and detailed.

Important issues—like liens or valuation gaps—can be buried in the report.

AI can:

Highlight potential risks

Flag issues that may impact approval

Connect findings to relevant guidelines

So nothing important gets missed.

Scenario 4: Preparing a Clean Submission

One of the biggest challenges is getting the file “submission ready.”

AskBob can:

Review the full file

Identify gaps or inconsistencies

Suggest what needs to be addressed before underwriting

Which leads to:

Fewer conditions

Faster approvals

Better turn times

The Shift: From File Chasing to File Confidence

In many mortgage operations today, processing is still largely reactive. A file comes in, issues are discovered, conditions are requested, and by the time those are addressed, new problems often appear. Much of a processor’s day becomes an ongoing cycle of chasing documents, clarifying guidelines, and fixing issues that could have been identified earlier.

AI begins to change that dynamic. Instead of constantly reacting to problems, processors start with a clearer, more complete file. Missing items are flagged earlier, guideline questions are answered faster, and submissions arrive better structured. The role shifts from constantly managing chaos to managing a smoother, more predictable workflow—moving processors away from file chasing and toward file confidence.

How AI Actually Creates Value in Processing

AI as a Throughput Multiplier

Most processing teams don’t struggle because of talent. They struggle because of volume.

As loan production increases, so does the workload:

More documents to review

More borrower and loan officer follow-ups

More opportunities for mistakes in the file

The problem is that staffing rarely grows at the same pace as loan volume. This is where AI helps. Instead of replacing processors, it reduces the amount of manual review required and surfaces issues earlier in the file.

The result is simple: processors can manage more loans while maintaining strong file quality and reducing risk.

Why Data Still Matters for Mortgage Processors

AI is powerful—but it’s only as good as the information behind it. For mortgage processors, that means the quality and completeness of the documents in the file still matter. If documents are inconsistent, missing, or incomplete, AI won’t magically repair the problem.

What it will do is surface those gaps immediately. And that’s actually a benefit.

Because when mortgage processors can see issues earlier in the file, they can correct them faster—resulting in stronger submissions, fewer conditions from underwriting, and a smoother path to closing.

The Learning Curve Is Simpler Than You Think

Processors don’t need to learn how AI works. They just need to use it in the flow of their work.

Start with:

Document validation

File completeness checks

Pre-submission review. From there, you’ll quickly see where it adds value.

What Mortgage Processors Should Do Now

Start by applying AI to the most time-consuming parts of your workflow.

Use it to validate documents as they come in.

Use it to prepare cleaner submissions.

Use it to reduce back-and-forth before underwriting.

That’s where the immediate impact is.

Final Thought

AI won’t replace mortgage processors, but it will redefine what great processing looks like. The advantage will come from cleaner files, faster submissions, and fewer surprises in underwriting. Instead of chasing documents and fixing issues late, processors will operate with clarity from the start. And the teams that win will be the ones who turn processing from a bottleneck into a competitive advantage.

FAQ: AI for Mortgage Processors

How can AI help mortgage processors?

AI helps processors by validating documents, identifying missing information, flagging inconsistencies, and preparing cleaner loan files for underwriting.

Does AI replace mortgage processors?

No. AI supports processors by reducing manual work and improving file quality, but human coordination and judgment remain essential.

What are the biggest benefits of AI in mortgage processing?

Faster turn times, fewer conditions, improved file quality, and reduced back-and-forth between teams.

Can AI reduce underwriting conditions?

Yes. By identifying issues earlier in the process, AI helps ensure files are more complete before submission, reducing conditions.

What is the best way for processors to start using AI? Start with document validation and pre-submission checks, then expand into broader workflow support as you see results.

Photo Credit Deagreez